So many people come to our offices for the first time in their 40s, 50s, and beyond, feeling a little or very embarrassed. They think it’s too late; they’ve put off getting their financial house in order for so long, preparing for retirement, having any plan at all. But no matter when someone comes in, the important, magical gift they are giving themselves will pay off. It is not too late.

To your Prosperity!

Aaron Wade, Kasey Claytor, Dawn Lopez, & Kelsey Bartholomew

One of the things that makes the annual March Madness college basketball tournament so fun to watch is the way so many games go down to the wire. As long as there is time left on the clock, the team that’s behind still has a chance to win.

And with the final seconds of the game running out, it’s amazing to see how teams will methodically run their well-rehearsed play to set up the winning shot. When time is short, discipline pays off.

This is true for basketball and saving for retirement.

Generation X, typically defined as those born between 1965 and 1980, is the next cohort to reach retirement age. Unfortunately, with time running out for building their nest egg, only about 1 in 7 Gen Xers think they have enough saved.

Recent research from wealth management firm Schroders reveals that only 14% of Americans aged 44 to 59 believe they’ve saved enough for retirement.1 And when compared to other generations, Gen Xers are more pessimistic about their ability to achieve their dream retirement, and more worried about outliving their retirement savings.

The reality is that many (if not most) people in their mid-forties to late fifties have not saved enough for a comfortable retirement. They came of age in a time when “defined benefit” plans like pensions were being replaced by “defined contribution” plans like 401(k)s, but before automated features made early, aggressive saving the default.

However, there is hope for this generation. In the past decade, federal legislation has made it easier to prioritize saving and has created special catch-up rules to help people get back on track in the years leading up to retirement.

A key finding in the Schroders study is how few of Gen X are seeking professional help. Only about half say they have done any kind of retirement planning. And only about a quarter (27%) are working with an advisor.

One of the lessons you’d hope those in their forties and fifties would have learned is that when you believe you have a major problem, get professional help. Then you’ll know the true extent of the issue and can take informed action toward solving it. Both of which reduce your worry about it.

When it comes to saving for retirement, your trusted advisor plays a dual role. First, he or she analyzes your current situation (income, debt, and everything that affects your finances), helps you define your goals for retirement, and then creates a flexible plan to reach those goals. Second, he or she provides the encouragement and accountability you need to meet your milestones along the way.

As long as you have time, you still have a chance for retirement success.

Disclosure: The views expressed herein are exclusively those of Efficient Advisors, LLC (‘EA’), and are not meant as investment advice and are subject to change. All charts and graphs are presented for informational and analytical purposes only. No chart or graph is intended to be used as a guide to investing. EA portfolios may contain specific securities that have been mentioned herein. EA makes no claim as to the suitability of these securities. Past performance is not a guarantee of future performance. Information contained herein is derived from sources we believe to be reliable, however, we do not represent that this information is complete or accurate and it should not be relied upon as such. All opinions expressed herein are subject to change without notice. This information is prepared for general information only. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. You should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. You should note that security values may fluctuate and that each security’s price or value may rise or fall. Accordingly, investors may receive back less than originally invested. Investing in any security involves certain systematic risks including, but not limited to, market risk, interest-rate risk, inflation risk, and event risk. These risks are in addition to any unsystematic risks associated with particular investment styles or strategies.

The markets are volatile right now, which isn’t surprising due to the extreme headlines. Many of you who have cash sitting on the sidelines may think this certainly is not a good time to invest. Is it?

There are ways to mitigate the risks of down markets. One is a strategy called dollar cost averaging. It is one way you can benefit from the volatility. By systematically adding to your account, either monthly, quarterly, or yearly, you are buying when stocks are high and low, giving your cost basis the benefit by buying more shares when the stock prices are down. As the market recovers, you have more shares going up.

It is simple but effective. That’s one reason your 401k is so successful. It works well in these types of markets! If you are going into the market today, you could set it up to invest it in a few lump sums. This is one of those advantageous times. Something to think about.

To your Prosperity!

Aaron Wade, Kasey Claytor, Dawn Lopez, & Kelsey Bartholomew

Aaron and Kasey just returned from a brief conference in California hosted by AssetMark. Big changes for us, and we think it will be a big net positive for you, our clientele. We’re so excited to share an abundance of information over the next couple of months. Not much will change from what you will see, unless you choose to participate in the new offerings.

Below, we’re sharing a brief list of the information we received last Thursday.

On a housekeeping note, as we mentioned before, if you need to ask a question, withdraw money, set up new instructions, or do anything related to your accounts, the best practice is always to call the office. Sending us instructions via email or text is unreliable. They may never reach your intended advisor, as they may end up in junk mail or similar folders. We may be away from the office, but someone is there to answer the phone during our open hours. We get hundreds of emails daily, so you can imagine!

From the CEOs of AssetMark down to the staff we met, mingled with, and listened to, we learned so much. We heard of their principles, intentions, and practices. We were impressed with the company’s history and its emphasis on making our clients’ experience a top priority. They understand our focus is on our clients, that you value the trust and reliability of advisors who know your priorities, the service you want, and the care provided to your managed accounts.

Many of you have been with us through changes before, and we have always told you we would only change if it meant our clients would benefit more by doing so.

Here is a list of some of the benefits coming up.

More investment products. Expansive platform. Industry-recognized due diligence team.

Tax management service on all investment solutions

More portfolios to choose from, more investment companies.

A charitable fund across all custodians

More reports available

More services to us, the advisors for operations, with a dedicated fast response team.

We will have access to in-house estate planning attorneys.

As always, when we adopt new looks or add new online features/sites, please contact us with any questions or concerns.

This is just a quick note to remind you of a few things about investing. We’ve had a great year so far. The markets are hitting new highs; the accounts are showing significant returns, and everyone is pretty happy.

To invest in the stock and bond markets, you must have emotional resilience. That is to say, it takes little discipline to stay with your investments when returns are positive. We all know the markets do not just keep going in one direction. Markets are volatile. We will have a correction; the markets will go down at some point. No one knows what will precipitate it. But it will be something that causes anxiety, fear, and worry.

It will be temporary. It always is. It is important to keep in mind that when stocks go up so much, we take some off the table and diversify them, such as moving some into bonds. When stocks fall enough, we begin purchasing more at lower prices. This is the old standby rule: buy low, sell high. This is called rebalancing, adjusting the portfolio to your target allocation.

We’ve been through a lot of them — some minor, some major — over the years. One thing that builds resilience is knowledge.

We are here to answer any questions you have. If you’d like a review of your account, give us a call.

To your Prosperity!

Aaron Wade, Kasey Claytor, Dawn Lopez, & Kelsey Bartholomew

There is always good news and bad news. However, we rarely tune in or log in to find good news. This tends to give us the impression that things are worse than they really are. And then you have ads harking how bad the economy is, how scary, how you need their information, products, and services to stay safe!

It is pretty disappointing to observe how those who benefit from scaring us behave.

This is one of the ways we earn our pay. Being the voice of reason. The markets are fine, trading is normal. Earnings season is upon us, and doing quite well. Corporations are surviving, albeit they need more trade jobs filled.

Short-term market movements are reacting to current news. It is short-lived. In the long term, they are meaningless. When we follow 5 and 10 year rolling periods, it smooths out the up-and-down jumps. We have occasional down markets and some bear markets. The strength of the stock markets and the economy is as strong as that of our citizens, our workers, and our companies, both large and small. We bet on that. Not what ads say.

The feature below also discusses the positive performance of global markets. I bet you didn’t hear about that!

To your Prosperity!

Aaron Wade, Kasey Claytor, Dawn Lopez & Kelsey Bartholomew

The Global Rally Many Investors Didn’t See Coming

July 17, 2025 — For the first time in over a decade, international equities have decisively outpaced U.S. stocks in the first half of 2025, marking a significant shift in global market dynamics. The MSCI All Country World Index ex USA has gained 17.3% year-to-date, outpacing the S&P 500’s 9.8% rise.

A World of Opportunity: Regional Market Spotlights

Germany — The Comeback of the Manufacturing Powerhouse Germany’s DAX 40 is up 19% YTD, bolstered by a recovery in industrial exports and a green energy push that has attracted global capital. German automation firms and renewable energy leaders have driven much of this growth.

France — Tech and Luxury Lead the Charge The CAC 40 gained 16%, powered by robust performance in luxury brands like LVMH and Hermès, alongside a vibrant tech sector centered around Paris’s startup ecosystem, now dubbed “Silicon Seine.”

Japan — Corporate Reform Unleashes Value Japanese equities have attracted both domestic and foreign investors as corporate governance reforms deepen. Companies increasing dividends and share buybacks have propelled the Nikkei’s 22% surge.

Brazil — Commodities and Infrastructure Boom Brazil’s Bovespa climbed 24%, driven by strong global demand for critical minerals and agricultural exports. Major infrastructure projects, backed by both government and foreign investors, have provided an additional boost.

India — The AI Supply Chain Winner India’s Sensex hit new highs with a 21% increase, benefiting from its growing role in global AI hardware manufacturing and services. The government’s tech-forward economic policies continue to attract multinationals and venture capital.

Bottom Line

Markets remain unpredictable. While U.S. stocks have still performed historically well so far this year, 2025 is serving as a timely reminder of the importance of maintaining a diversified investment approach in an ever-changing market landscape.

Disclosure: The views expressed herein are exclusively those of Efficient Advisors, LLC (‘EA’), and are not meant as investment advice and are subject to change. All charts and graphs are presented for informational and analytical purposes only. No chart or graph is intended to be used as a guide to investing. EA portfolios may contain specific securities that have been mentioned herein. EA makes no claim as to the suitability of these securities. Past performance is not a guarantee of future performance. Information contained herein is derived from sources we believe to be reliable, however, we do not represent that this information is complete or accurate and it should not be relied upon as such. All opinions expressed herein are subject to change without notice. This information is prepared for general information only. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. You should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. You should note that security values may fluctuate and that each security’s price or value may rise or fall. Accordingly, investors may receive back less than originally invested. Investing in any security involves certain systematic risks including, but not limited to, market risk, interest-rate risk, inflation risk, and event risk. These risks are in addition to any unsystematic risks associated with particular investment styles or strategies. You cannot invest directly in an index.

Happy Friday, everyone! This article reminds us of all the potential problems that financial planning and investing mistakes can cause. We realize no one is perfect, but there are safeguards that can be instituted so you can feel confident in your retirement and estate planning decisions.

We can help. Just give us a call. And an added gift to you is our Osprey Estate Planning Organizer to download here!Print it out. Put one in your safe deposit box, give one to your executor or successor trustee, and make their job easier.

To your Prosperity!

Aaron Wade, Kasey Claytor, Dawn Lopez & Kelsey Bartholomew

A friend of ours was lamenting how slow and costly it was to sort out his parents’ estate after they had both passed away. His father thought that by setting up a trust, everything would be easily distributed to his heirs.

Unfortunately, our friend and his siblings found out that there were lots of loose ends their father hadn’t taken care of—things he wasn’t even aware he was supposed to do. For example, he had money in an investment account that wasn’t included in the trust and didn’t have named beneficiaries. As a result, his children were going to have to spend considerable time and money to send it through probate.

Our friend is convinced these were things that would all have been taken care of (or at least planned for) if his father had worked with a financial advisor. His dad was a highly intelligent man with good intentions. But what he didn’t know cost his kids thousands in unnecessary taxes and legal fees.

But it’s not just in estate planning where ignorance comes at a high cost.

Laura Beck writes in Yahoo!Finance about her conversation with a retiree who didn’t use an advisor, but now sees significant ways professional help could have greatly impacted his finances. She identifies him only as Wes B. (probably to save embarrassment).

One area where Wes B. realized he should have worked with an advisor was in saving for retirement. He thought he was being smart by putting money only in investments he understood, like the stock of the company he worked for. Now he realizes that his misunderstanding of risk led him to put too many eggs in one basket.

Another area Wes now wishes he’d had help in was timing when to take Social Security. He thought it was a no-brainer to start getting the benefit as soon as he was eligible at age 62. He made this decision, in part, because of his mistaken assumptions about his own predicted longevity. Now he sees it as a costly mistake.

But the biggest way Wes B. is now convinced an advisor could have helped him was in planning for unexpectedly big costs in retirement, such as healthcare and taxes. He thought Medicare would cover everything and that retirees didn’t have to pay taxes.

He told Beck that he made costly mistakes in all these areas—mistakes he could have avoided if he had sat down with an advisor.

Our friend with the challenging estate process put it this way: “An advisor’s job isn’t to help you ‘game’ the market for an extra thousand bucks. They’re there to keep you from making that $50,000 mistake.”1

And as our friend can attest, those mistakes are easy to make.

Your trusted advisor is there to help make sure your journey from wealth accumulation to retirement to passing along your estate goes according to a carefully considered plan. Taking steps today to prepare and plan with a competent professional can help both you and your loved ones achieve the financial wellbeing you desire.

The views expressed herein are exclusively those of Efficient Advisors, LLC (‘EA’), and are not meant as investment advice and are subject to change. All charts and graphs are presented for informational and analytical purposes only. No chart or graph is intended to be used as a guide to investing. EA portfolios may contain specific securities that have been mentioned herein. EA makes no claim as to the suitability of these securities. Past performance is not a guarantee of future performance. Information contained herein is derived from sources we believe to be reliable, however, we do not represent that this information is complete or accurate and it should not be relied upon as such. All opinions expressed herein are subject to change without notice. This information is prepared for general information only. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. You should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. You should note that security values may fluctuate and that each security’s price or value may rise or fall. Accordingly, investors may receive back less than originally invested. Investing in any security involves certain systematic risks including, but not limited to, market risk, interest-rate risk, inflation risk, and event risk. These risks are in addition to any unsystematic risks associated with particular investment styles or strategies.

Having walked my clients through planning, approaching, and living in retirement financially for the last almost 40 years, I couldn’t help but pick up on other aspects facing us besides the money part, such as grappling with when to retire, what to do in retirement, and how to plan a full and thriving last third of life. As I heard someone say, “What are you going to do between now and death?”

As we near our ‘golden years,’ we observe our elders living in a great variety of ways, from scrapping by on social security to cruising or flying around the world and traveling between multiple homes. There is an undeniable correlation between financial health and satisfaction in the later years, but this doesn’t mean you need to be stinking rich.

A successful retirement appears to have several moving parts: financial, health and wellbeing, relationships, passions, and purpose. Let’s face it: Nearing death also affects one’s beliefs and how one experiences one’s spiritual life. So, how do we prepare ourselves for this last and significant period of our lives?

First, not planning for it or setting goals, not contemplating how you will live in retirement, can cause unnecessary suffering later on. With no plan, no savings, and with no interests outside of work, some retirees may end up spinning in their own exhaust, nowhere to go and nothing to do. This can be disastrous for the human spirit. Depression and other mental health problems can take hold, leading to unhappiness and even physical ailments. But let’s not dwell on this because the fact that you are reading this means you are proactive, interested, and willing to learn. Yay, you!

This topic could easily be a 400-page book, but I will give you the briefest of outlines here.

1) Financially

Never too early or too late to begin saving. Have your paycheck debited for your employer plan, or have your checking account systematically debited to go into an IRA, as much as you can afford, and then a little more.

Invest in a broad, diversified portfolio with stocks and bonds, low fees, and comprehensive management.

Beware if you have the tendency, like some parents of adult children, to financially help them to such an extent that you harm your own comfortable retirement. I remember a client who borrowed against his home and withdrew from his IRAs to help a daughter who said she couldn’t find a job. He did this until he and his wife had to give up their plans to travel with their friends in retirement. He died leaving nothing for his wife, and only after his death did his daughter go to work to support herself.

We used to say that in the financial business in the 1980s, you needed at least as much in savings as your closest decade, a hundred thousand dollars for each. For instance, at 40 years old, you should have saved $400,000; at 60, $600,000; and so on. Typical standards now in financial planning state are that it really takes much closer to one million to have financial freedom these days to enable no financial worries and the ability to take care of all your needs. Yet, I have seen people retire with half that and get along just fine.

Educate yourself on how money and the markets work. Call our office at 321-383-4005 for our 30-page booklet on the 7 Big Mistakes Investors Make and the 7 Habits of Successful Investors to get you started.

2) Health and Wellbeing

Of course, take good care of yourself. Eat a good, healthy diet with lots of fresh vegetables, fruits, nuts, and lean proteins.

Get outside every day. Walk, bike, swim, play, explore, move. Take up yoga or Tai chi, dancing, or some other social exercise. These good habits will be easy to follow into retirement. With good balance, falls become much less likely, among many other benefits.

Find a mindfulness practice you like, such as meditation, contemplation, breathing techniques, prayer, and self-reflection. Conditioning the mind for well-being is also essential.

If you do have anxiety, depression, or other emotional problems bothering you, find a good therapist. Most of these issues are resolved with the proper help. Our society still attaches an unfortunate stigma to getting assistance in this area, but it is so essential, shows emotional maturity and self-care, and can be a rewarding experience.

Develop a positive attitude toward aging and retirement. Daydream about all the activities and experiences you’ll be able to enjoy and the friends and family with whom you will spend time. If you don’t have a close circle of friends, join a club or a class. Get involved in something you enjoy, sports, a book club, knitting, hiking, etc., and read; I can’t stress how much reading can enhance anyone’s life in so many ways. There are so many great books in the self-help genre, but even a great book of fiction is a positive experience.

Cultivate peace with your own passing. Our cultures in the West have a poor record of coming to terms with death. It’s not usually spoken about except in dramatic and negative ways; we pretend it isn’t inevitable; we try to extend the lives of our loved ones in often grotesque and extreme ways, making their last days, weeks or months lying in a sterile facility hooked up to machines and on heavy medications. My recommendation is to have a good plan. Most states have a Dying with Dignity form to fill out, describing what you want to be done and how in a terminal situation. Let us know if you would like us to mail you one. Other than this, building a solid belief of your own, whether religious or faith in life and nature, can reframe the end of life as something not to fear. There are many great books on this.

3) Relationships

Fostering good relationships takes time, effort, and the ability to forgive—maybe yourself or others. We all say or do things we don’t mean at times, and we are hurt by others’ words or actions. Without processing these productively, we can be emotionally drained, hurt, or worse. Forgive yourself and others. I know it’s hard. I will never forget a ninety-six-year-old, long-time client on his deathbed telling me he had been too hard on his wife and children. He was verbally abusive. He carried this all of his life. If he had been self-reflective, brave enough to look within, and been able to forgive himself, he wouldn’t have been so full of pain at the end.

Approaching this last stage of life, we can take the opportunity to develop a positive relationship with ourselves and others that will nurture us.

4) Passions and Purpose

What do you envision doing during retirement? So many people have jobs they don’t enjoy, so they dream of retiring as soon as possible, looking forward to having endless free days, like permanent weekends. But they’ve spent little time thinking about what they will do in retirement. I’ve seen some retire in their 50s and become bored, aimless, and searching. Some go back to work. Some actually lose interest in life.

On the other hand, I’ve seen people in their 70s who have no intention of retiring anytime soon because they love what they are doing.

Studies show that the more control you have over what you do at work, who you work with, and so on, the more satisfied you are. I believe that is why entrepreneurs often scoff at the idea of retiring; they are already living the life of their dreams.

To discover what your perfect retirement might look like, create a vision board of activities and places you’re interested in exploring. Think about what you enjoyed as a child.

Ask how you may serve your community.

5) Deciding When to Retire

So, I am guessing you are beginning to see that fiscal retirement is not just about what age you can retire; it is about so much more than that.

1) You want to retire when you are healthy and able to enjoy your passions

2) You’ve figured out how to fulfill your needs for community, purpose, interests, and activities.

3) Ensure you aren’t just continuing to work because you have no idea what else to do with your life. Maybe you aren’t totally satisfied with your work but haven’t invested the time to explore what else might interest you.

4) What about semi-retiring? This is becoming very popular for those who have this option. And if you don’t, perhaps you could retire and pick up a part-time job doing something you’ve always wanted to do, like teaching art or working in a counseling position.

5) Talk with your financial advisor about the income you will need during retirement. Consider the cost of your desired lifestyle, your social security, and the amount of investments it will take to produce the income.

These subjects require some introspection; knowing yourself well will help you plan your later years to your benefit. Settling into the idea of being an elder in the community, offering your hard-wrought wisdom, having loving relationships, enjoying the fruits of your labor, knowing how to still play, and exploring the world with a sense of wonder can make your retirement the best time of your life.

We hope this newsletter finds everyone safe and comfortable after this awful hurricane season in the Southeast. Our offices experienced outages, and the parking lot was a complete mess, but we were very lucky in our neck of the woods. We were glad we had just put a new roof on our old building.

Today’s article is regarding how an election might affect your portfolios. Let us know if you have any questions.

To your Prosperity!

Aaron Wade, Kasey Claytor, Dawn Lopez & Kelsey Bartholomew

How Much Do Elections Affect the Stock Market?

With the election just weeks away, you’ve probably seen some pretty dramatic predictions about what will happen to the economy if one side or the other wins. While the outcome of this particular election is hard to predict (not just nationally but also for state and local offices), economists have identified some market behavior that’s sure to occur. Just the fact that we’re having an election tends to increase uncertainty. Investors don’t like uncertainty. And so it tends to make them react more strongly to market information. “In the absence of a clear consensus about the (election) outcome,” writes economist Clive Walker, “we see larger daily price changes that seem to offset each other.”1 In other words, we might see bigger swings both up and down, but in the long run, stock prices will likely remain largely unchanged. Businesses also don’t like uncertainty. One study found that U.S. firms tend to reduce investment expenditures during election years, which can depress the market. On the other hand, older research suggests that politicians often attempt to boost the economy before elections. So again, a significant long-term effect seems unlikely to occur, much less persist for any meaningful time period. Uncertainty can continue after the election as everyone waits to see what new policies the winners will enact. These changes are most likely to affect industries that are sensitive to government spending, including sectors like healthcare, defense, and finance. Additionally, new tax policies will also have some effect. While politicians may promise a chicken in every pot and a new car in every garage, the economy is just too complex, and economic cycles are simply too long to guarantee immediate prosperity. However, economic promises resonate strongly with voters, so politicians are not going to stop making them. Knowing this, the prudent investor won’t be overly optimistic or overly worried about how the election will affect his or her portfolio. They will expect to see increased volatility, especially when the national race is so closely contested. They will expect the market to overreact in the short term while investors wait for the dust to settle. Elections are important. As free citizens, we have both the privilege and responsibility to vote. So, we encourage you to get out your voter’s guide and make your best-informed decision about who should be in charge of our local, state, and national governments.

Sources:1. http://go.pardot.com/e/91522/ctions-affect-the-stock-market/95p293/2481654251/h/S_rYvpDvTgMO47sOFIYrbtW1oJmFqALaz5WkCeWhXlM Disclosure:The views expressed herein are exclusively those of Efficient Advisors, LLC (‘EA’), and are not meant as investment advice and are subject to change. All charts and graphs are presented for informational and analytical purposes only. No chart or graph is intended to be used as a guide to investing. EA portfolios may contain specific securities that have been mentioned herein. EA makes no claim as to the suitability of these securities. Past performance is not a guarantee of future performance. Information contained herein is derived from sources we believe to be reliable, however, we do not represent that this information is complete or accurate and it should not be relied upon as such. All opinions expressed herein are subject to change without notice. This information is prepared for general information only. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. You should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. You should note that security values may fluctuate and that each security’s price or value may rise or fall. Accordingly, investors may receive back less than originally invested. Investing in any security involves certain systematic risks including, but not limited to, market risk, interest-rate risk, inflation risk, and event risk. These risks are in addition to any unsystematic risks associated with particular investment styles or strategies.

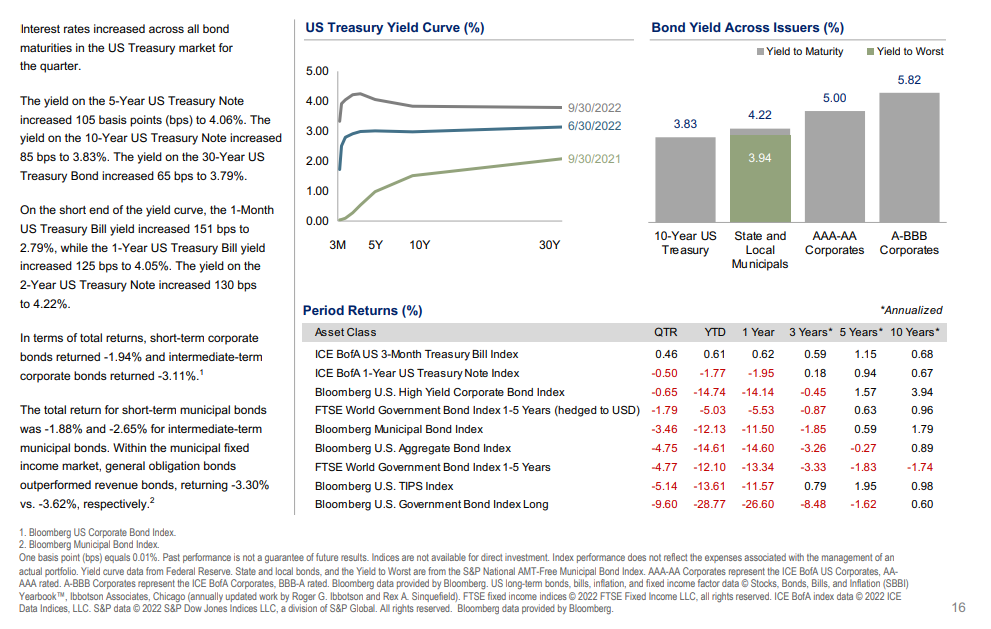

As Interest Rates Climb, are Bonds Still a Good Investment?

“The best protection against inflation is your own personal earning power. . . If you do something valuable and good for society, it doesn’t matter what theU.S. dollar does.” – Warren Buffett

The Federal Reserve has two main goals: to keep unemployment low and keep inflation low. They have basically one tool for achieving this: setting interest rates. Lately, unemployment has been low, but inflation has been running at its highest level in more than 40 years. Consequently, to bring it down by putting a damper on the economy, the Fed has continued its policy of increasing interest rates.

This course of action was seen as inevitable by those who believed the current round of inflation was not as “temporary and transitory” as many had hoped. As a result of this tightening of the money supply the stock market responded with a series of corrections which has resulted in another quarter of losses for all the major indexes.

Whether this latest round of rate hikes will finally slow inflation is yet to be seen. It certainly has participated in bringing down the prices of stocks. For this reason, those who believe the market will eventually return to its long-term trend of growth have been purchasing equities at a discount.

However, stocks are not the only widely traded instrument available to investors. Bonds are also a key component of a diverse portfolio. While they too have suffered under rising rates, they have a built-in mechanism which dampens their volatility.

The Bond Teeter-Totter

Bonds are instruments of debt instead of equity (like stocks) and have two components, which is why people often find them confusing. A bond is basically an IOU between a borrower (the government or corporation issuer) and a lender (the purchaser). As with a loan, the bond issuer agrees to repay the principal on a predetermined schedule and make interest payments along the way.

A bond can be bought and sold like a stock; therefore it has a market price. So, the two components of a bond are its value (market price) and its income return (interest payments).

Many factors can affect a bond’s price, including its duration (sensitivity to small interest rate changes) and the reliability of the issuer. For example, bonds with a higher risk of default are called junk bonds and have a higher return as a result.

Another significant factor in the price of a bond is a change in interest rates. When a high-quality bond is issued, its return will be in line with current interest rates. For example, let’s say a bond was issued when rates were at 2%. When the Fed raises interest rates to 2.25%, that 2% return becomes less attractive. After all, you can buy new bonds with higher returns. In turn that original bond’s price drops until its return reflects the new higher rate.

Here’s how that would work with a 10-year bond worth $100 that pays 2%. Interest rates rise to 2.25%. That bond will drop to $80 in value, because at that lower price $100 worth will now pay 2.25%.

This teeter-totter effect tends to balance out the loss in market value. Of course, like stocks, you only realize a loss when you sell a bond.

Bonds have this built-in mitigating factor and a predetermined term and return, because of this they tend to be less volatile than stocks. Of course, that lower risk produces lower returns on average. However, when stocks are taking a beating, investors find the relative safety of bonds more attractive, and their prices go up. On the other hand, when stocks are soaring, investors find lower- performing bonds less attractive, and they fall in value.

In general, stocks and bonds tend to move in opposite directions, which makes owning both an attractive tactic in an overall strategy of holding a diverse portfolio. Since the movements of the market are unpredictable, the most prudent strategy is to own instruments that allow you to benefit from unexpected gains, while limiting your exposure to unexpected losses.

The big events that affect the global market are so unpredictable—events like the pandemic, the Great Resignation, and the war in Ukraine. So, it makes sense to follow a plan that’s designed for the long-term.

Who knows what surprises will be in store for investors this next quarter?

But we can be sure that investors who worry less about what they can’t control, and focus more on the things they can, will be much better off in the long run.

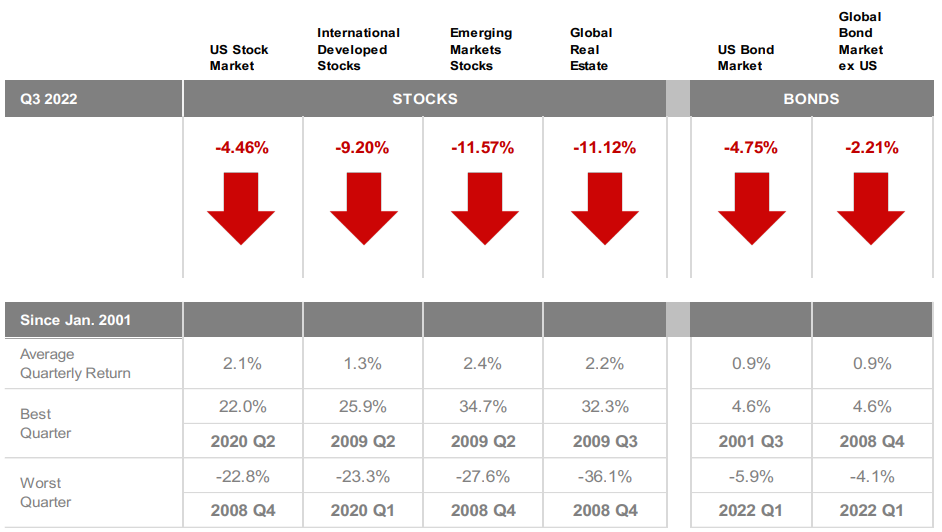

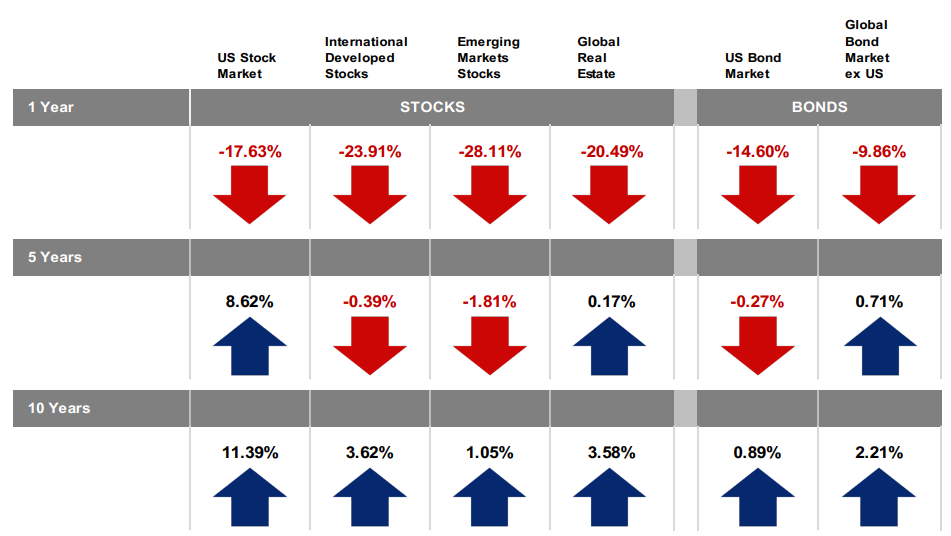

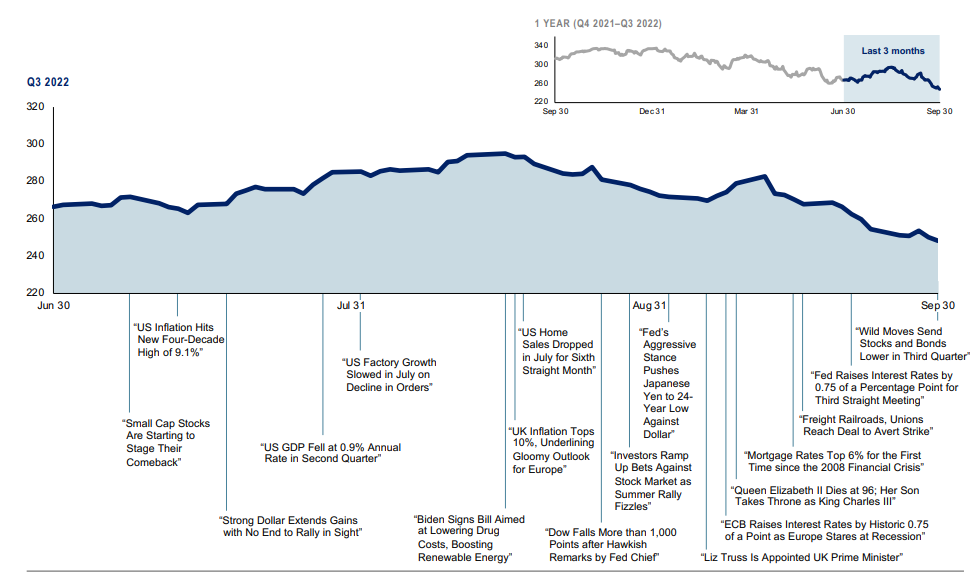

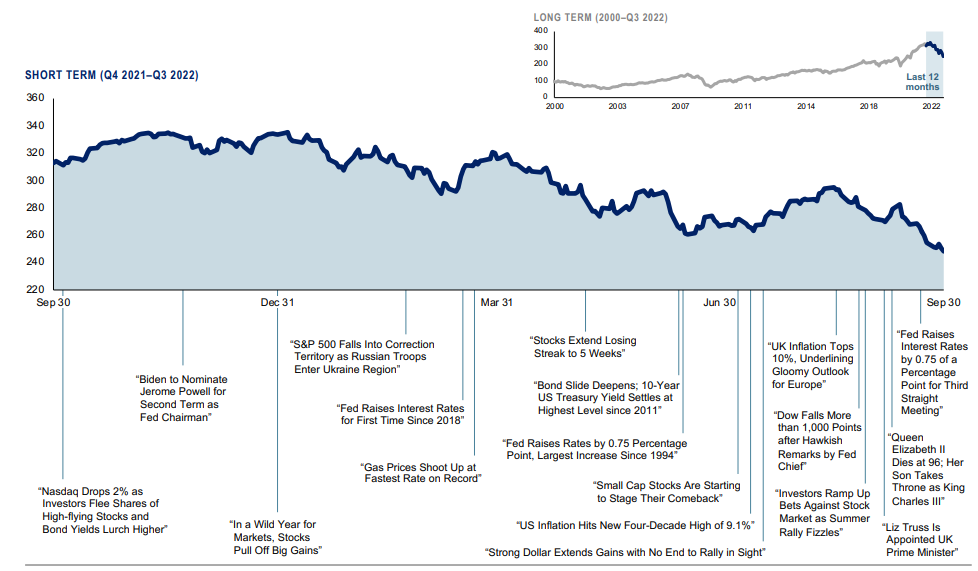

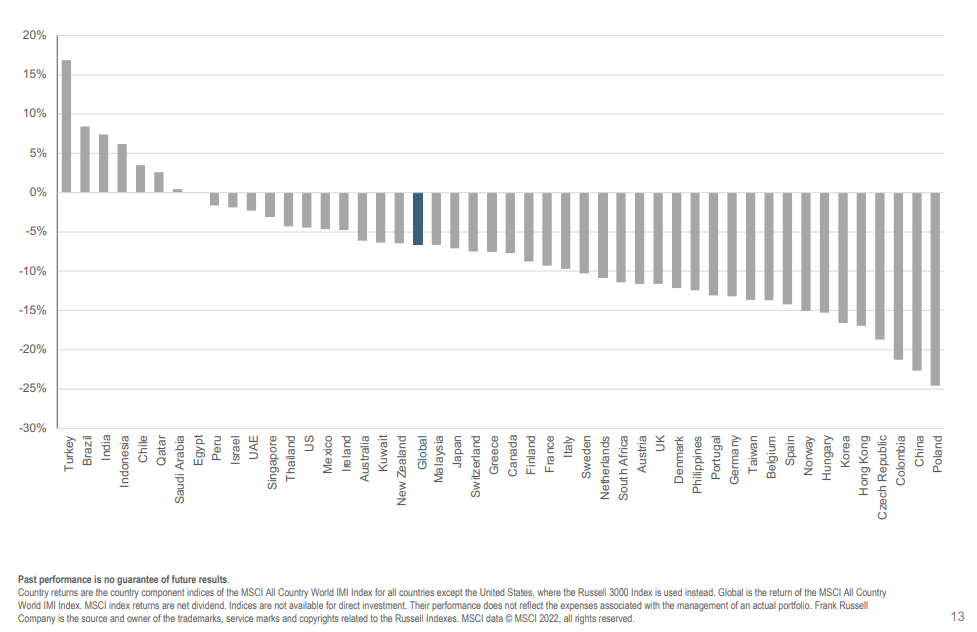

MSCI All Country World Index with selected headlines from Q3 2022

These headlines are not offered to explain market returns. Instead, they serve as a reminder that investors should view daily events from a long-term perspective and avoid making investment decisions based solely on the news.

MSCI All Country World Index with selected headlines from past 12 months

These headlines are not offered to explain market returns. Instead, they serve as a reminder that investors should view daily events from a long-term perspective and avoid making investment decisions based solely on the news.

What Drives Investment Returns? Start with Ingenuity.

Third quarter 2022

A recent news item reported that Frederick Smith intended to step down as Chairman and Chief Executive Officer of FedEx Corp., the largest air freight firm in the world.

As a Yale undergraduate in 1965, Smith wrote a term paper for his economics course outlining an overnight air delivery service for urgently needed items such as medicines or computer parts. His professor was not much impressed with the paper, but after a stint in the Air Force, Smith sought to put his classroom idea into practice. He founded Federal Express (now FedEx) in 1971, and one evening in April 1973, 14 Dassault Falcon jets took off from Memphis airport with 186 packages destined for 25 cities.

In retrospect, it was not an auspicious time to launch a new venture requiring expensive aircraft consuming large quantities of jet fuel. Oil prices rose sharply later that year following the Arab states’ oil embargo, and the US economy fell into a deep recession. Most airlines struggled during the 1970s, and Federal Express was no exception.

But Smith’s idea found favor with customers, and 49 years after its initial deliveries, the firm is a global colossus with over 650 aircraft, including 42 Boeing 777s—each of which can fly more cargo than 100 Falcons. Although it took over two years to turn its first profit, FedEx became the first start-up in American history to generate over $1 billion in revenue in less than 10 years without relying on mergers or acquisitions. The journey has proved rewarding for investors as well—100 shares purchased at the initial offering price of $24 in 1978 has mushroomed to 3,200 shares worth over $718,000 as of May 31, 2022.1

Fred Smith’s idea is just one example of ingenuity that humans have exhibited for centuries. Sticks and stones led to hammers and spears, the wheel and axle, the steam engine, and eventually semiconductors and jet aircraft. The invention of writing made it possible to store and hand down information from one generation to the next, enabling ingenuity to compound into an ever-increasing body of knowledge.

Although we often associate innovation with clever new technology, some remarkable developments have required little more than astute powers of observation. The curse of smallpox, for example, has afflicted humans with death or disfigurement for thousands of years. English doctor Edward Jenner noticed that milkmaids who had previously experienced cowpox did not catch smallpox, and in 1796, he took material from a milkmaid’s cowpox sore and inoculated James Phipps, the nine-year-old son of his gardener. Later exposed to the virus, Phipps never developed smallpox, and Jenner published a treatise on vaccination in 1801. Smallpox vaccines gradually eliminated the disease in countries around the world, and the last known case was reported in Somalia in 1977.

Stock split information sourced from FedEx investor relations website. Stock price information provided by Bloomberg. This is not taking into account cash dividends or any reinvestment.

What Drives Investment Returns? Start with Ingenuity.

(continued from page 16)

One innovation often paves the way for others: • Charles Lindbergh took off from Long Island for his historic transatlantic flight to Paris on May 20, 1927. That same day, J. Willard Marriott opened a nine-stool lunch counter serving cold A&W root beer in Washington, D.C. Ten years later he began to supply box lunches to airlines flying from nearby Hoover airport and 20 years later opened the world’s first motor hotel in Arlington, Virginia. Today, Marriott is the world’s leading travel firm, with over 8,000 hotel properties in 139 countries. • The now-ubiquitous microwave oven can trace its roots to a happy accident. While working on radar equipment in 1945 for Massachusetts-based Raytheon, electronics engineer Percy Spencer noticed that the chocolate bar in his pocket had suddenly melted. His curiosity led to the introduction of commercial-grade water-cooled microwave ovens in 1947 costing thousands and ultimately to countertop units available today for $99. • Frustrated by lengthy delays associated with loading and unloading cargo ships, trucking firm owner Malcolm McLean launched a shipping service in 1956 using standardized steel containers of his own design. Met with great skepticism when first introduced, his idea for theftproof stackable cargo boxes eventually transformed the global shipping industry—and world trade—by slashing dockside loading costs over 90%. • On June 26, 1974, cashier Sharon Buchanan inaugurated the era of barcode inventory tracking when she scanned a pack of Juicy Fruit gum bearing a Universal Product Code at Marsh Supermarket in Troy, Ohio. Barcode scanners eliminated the drudgery and inevitable mistakes associated with manual entry by checkout clerks and provided store managers with powerful tools to track sales trends. As retailers such as Home Depot, Ross Stores, and Walmart expanded throughout the country in recent decades, barcode technology played a key role in matching inventory with local preferences at each location. • In March 2022, a 20-year-old woman born with a small and misshapen right ear received a 3D-printed ear implant made from her own cells and shaped to precisely match her other ear. Although experimental, the procedure represented a significant advance in tissue engineering and could eventually lead to artificial organs such as lungs or kidneys. The benefits of innovation are widely dispersed throughout the economy, often in unpredictable ways. Apple Inc. became one of the world’s most valuable companies based on its clever marriage of the computer and the telephone; both iPhone users and Apple shareholders reaped substantial rewards. On the other hand, suppose your fairy godmother had told you in 1935, at the dawn of commercial air travel, that this tiny sector of the economy would eventually become a gigantic industry with millions of passengers flying every year—including some flying from breakfast in New York to Los Angeles for dinner. What would your prediction be for industry pioneers such as TWA or Pan American? Most likely, bountiful prosperity and rewarding stock market performance. The millions of passengers materialized. The profits did not. Both firms went bankrupt. So innovation itself does not ensure prosperity in every case. That’s why it makes sense to diversify. Investors are often tempted to focus their attention on firms that appear poised to benefit from innovation. But it’s difficult to predict which ideas will prove successful, and even if we could, it’s unclear which firms will benefit and to what extent. Software giant Microsoft has been a big winner for investors, with the share value soaring more than 100-fold over the 30-year period ending May 31, 2022. Discount retailer Ross Stores proved even more rewarding, as the stock price multiplied over 189 times during the same period. One firm developed powerful computer technology and the other applied it. Civilization is a history of innovation—curious minds seeking to improve upon existing ways of meeting mankind’s wants and needs. Public securities markets are just one example of such creativity, and they have a history of rewarding investors for the capital they supply to fund such innovation. But a significant fraction of the wealth created in public equity markets typically comes from only a small number of firms; therefore, we believe owning a broad universe of stocks is the most effective way to participate in the rewards of ingenuity and innovation, wherever and whenever it takes place.

Investments involve risks. The investment return and principal value of an investment may fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original value. Past performance is not a guarantee of future results. There is no guarantee strategies will be successful. Named securities may be held in accounts managed by Dimensional. This information should not be considered a recommendation to buy or sell a particular security. The information in this material is intended for the recipient’s background information and use only. It is provided in good faith and without any warranty or representation as to accuracy or completeness. Information and opinions presented in this material have been obtained or derived from sources believed by Dimensional to be reliable, and Dimensional has reasonable grounds to believe that all factual information herein is true as at the date of this material. It does not constitute investment advice, a recommendation, or an offer of any services or products for sale and is not intended to provide a sufficient basis on which to make an investment decision. Before acting on any information in this document, you should consider whether it is appropriate for your particular circumstances and, if appropriate, seek professional advice. It is the responsibility of any persons wishing to make a purchase to inform themselves of and observe all applicable laws and regulations. Unauthorized reproduction or transmission of this material is strictly prohibited. Dimensional accepts no responsibility for loss arising from the use of the information contained herein. This material is not directed at any person in any jurisdiction where the availability of this material is prohibited or would subject Dimensional or its products or services to any registration, licensing, or other such legal requirements within the jurisdiction. “Dimensional” refers to the Dimensional separate but affiliated entities generally, rather than to one particular entity. These entities are Dimensional Fund Advisors LP, Dimensional Fund Advisors Ltd., Dimensional Ireland Limited, DFA Australia Limited, Dimensional Fund Advisors Canada ULC, Dimensional Fund Advisors Pte. Ltd., Dimensional Japan Ltd. and Dimensional Hong Kong Limited. Dimensional Hong Kong Limited is licensed by the Securities and Futures Commission to conduct Type 1 (dealing in securities) regulated activities only and does not provide asset management services. Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission. Investment products: • Not FDIC Insured • Not Bank Guaranteed • May Lose Value Dimensional Fund Advisors does not have any bank affiliates

Disclosures

Efficient Advisors, LLC (“Efficient”) is an SEC-registered investment adviser that provides discretionary asset management to individuals, corporations, and trusts. Registration neither implies an endorsement by the SEC nor connotes a specific level of skill or training. Efficient uses exchange traded funds (ETFs) and mutual funds to provide globally diversified, structured investment portfolios to its clients. The information presented here has not been approved or verified by the United States Securities and Exchange Commission or by any state securities authority.

Please note that the models discussed in the presentation are designed to illustrate the benefits of global diversification and do not represent actual Efficient Advisors’ portfolios. Investors should carefully consider the investment objectives, risks, charges and expenses of the Efficient Advisors’ Portfolios prior to investing. This and other important information about Efficient can be found in Efficient’s Disclosure Brochure and at www.adviserinfo.sec.gov. All investments involve risk, including the loss of principal. Past performance is not a guarantee of future results. Investments in securities are subject to volatility, or in other words, subject to rapid or unexpected changes. Future performance may be less than, equal to, or greater than past performance. An investor and his financial advisor should discuss risk, volatility and possible ways to lower exposure to risk and volatility. Risk can be systematic, also known as market risk, and nonsystematic. Systematic risk affects the economy and securities markets as a whole. Systematic risk includes risk such as liquidity risk, inflation risk, interest-rate risk, and sociopolitical risk.

Nonsystematic risk is linked to investment in a particular industry sector or company. Types of nonsystematic risk include management risk and credit risk. ETFs and mutual funds are designed to mitigate systematic and nonsystematic risk by diversification, but remain subject to these risks. ETFs and mutual funds will have similar risks as well as other risks, such as investment management strategy risk. In Efficient’s managed portfolios, Efficient attempts to mitigate these risks by broadly diversifying the allocation across multiple asset classes of stocks and bonds, in both the US domestic and International markets. Efficient applies a disciplined, long-term, structured investment methodology and does not react to the emotional temptation to alter allocations due to short-term market volatility.

Performance and benchmark results are provided exclusively for illustrative purposes. The hypothetical results shown were achieved by means of back testing a hypothetical portfolio of representative indices for each asset class. The results assume annual rebalancing of the portfolios, the reinvestment of dividends and capital gains. The performance results do not reflect the deduction of transaction fees or custodial charges. Management fees are also excluded, unless specifically denoted, since this is a hypothetical illustration using indexes to demonstrate the benefits of diversification and does not represent actual Efficient Advisors portfolios. For information about the fees and expenses for Efficient’s portfolios, please review Efficient’s Disclosure Brochure.

Hypothetical performance results have certain inherent limitations. Hypothetical results are designed with the benefit of hindsight. For reasons including variances in portfolio account holdings (including the amount invested in cash), variances in the investment management fee incurred, market fluctuation, the date on which a client initiates an investment strategy, and any account contributions or withdrawals, the actual performance experienced by an investor may vary substantially from the indicated hypothetical performance results. Comparisons to benchmarks have limitations because benchmarks have volatility and other material characteristics that may differ from the portfolio(s) shown. Also, performance results for benchmarks do not reflect payment of investment management/incentive fees and other fund expenses. Because of these differences, benchmarks should not be relied upon as the sole measure of comparison. Unlike an actual performance record, simulated results do not represent actual trading. The results may under- or over compensate for the impact of various market and economic factors such as systematic and nonsystematic risk. No representation is being made that any account will or is likely to achieve future profits or losses similar to those shown. Investors should not assume that investment decisions Efficient makes in the future will be profitable or equal the investment performance of the past. Past performance does not indicate future results. You cannot invest directly in an index.

Merry Christmas andHappy New Year! We are wishing you the best health, happiness and prosperity going into 2022. In this issue is a great article for planning next year, and a good idea for a gift to give parents or grandparents; Kasey’s Will for leaving a legacy of stories and life lessons.

Our office schedule for the end of the year:

Closed Friday Dec. 24th to Friday December 31st for ChristmasReopening Monday January 3rd, 2022 We will be checking our mail and messages

To your Prosperity, Kasey Claytor, Aaron Wade and Dawn Lopez

Here comes 2022: Will history repeat itself? Whether we’re ready for it or not, 2022 will be here in a few days. Another year will have passed. You’ll look at your schedule, your finances, maybe even at the bathroom scale and wonder if this time next year you’ll be any closer to achieving the changes in your life you’d really like to make.Setting aside his politics for a moment, Karl Marx once wrote an interesting observation, “History repeats itself, first as tragedy, second as farce.”1 He was of course speaking of national events affecting millions of people. But the principle holds true in our personal lives as well. Our actions may cause us an unexpected setback. But then the next time we’re faced with a similar circumstance, we can’t seem to resist taking the same action again—even though we are fully aware of its detrimental outcome.Sales of expensive exercise equipment, scheduling planners, and weight loss apps soar in the first few weeks of January each year. People switch from indulging themselves to buying devices and memberships they hope will change how their conduct their lives.Unfortunately, these hoped-for transformations rarely take hold. Research has shown that willpower alone is not enduring enough to cause significant life change.2 It eventually gives out and the person goes back to their habit.The good news is that change is possible and the New Year is an excellent time to work for self improvement.Business coach Ashira Prossack has helped her clients find success by inserting a step before they make new resolutions, and that’s to spend time reflecting back on the year that is ending. The hustle of the holidays don’t make this easy.”With the end of the year fast approaching,” she writes, “it’s easy to feel overwhelmed. The holidays are often the busiest time of year, and there’s the added pressure of trying to finish up everything (at work) before December 31st.”3Prossack says you have to purposely set aside time to think back. But, she adds, at the end of the year you’re primed and ready to be in reflection mode.The next step, she advises, is to write out your goals for your personal life and career. Don’t worry yet about how you’ll accomplish them. Just get them down on paper. And be as detailed as possible.Finally, she says, write up your “game plan.” Identify the things you will need to do to accomplish your goals. And then list the specific steps you will need to take. The important thing is to write it all out. This will force you to think clearly about what it will take for you to accomplish your goal. If you break them down into small, easily doable tasks, you’ll be much better prepared to hit the ground running next year.And as far as financial goals, we would love to talk with you about what you’d like to accomplish over the next 12 months and how we can help you get there.Have a happy New Year and we will see you in 2022.

Sources:1. http://go.pardot.com/e/91522/quotes-karl-marx-382655/74zy66/1369296997?h=IVKKPIlyw5bi5djFDCIJmCOSLhSf3xorZg4Op_YEltg2. http://go.pardot.com/e/91522/-willpower-isnt-always-enough-/74zy68/1369296997?h=IVKKPIlyw5bi5djFDCIJmCOSLhSf3xorZg4Op_YEltg3. http://go.pardot.com/e/91522/usiness-success-new-year-2019-/74zy6b/1369296997?h=IVKKPIlyw5bi5djFDCIJmCOSLhSf3xorZg4Op_YEltgDisclosure:The views expressed herein are exclusively those of Efficient Advisors, LLC (‘EA’), and are not meant as investment advice and are subject to change. All charts and graphs are presented for informational and analytical purposes only. No chart or graph is intended to be used as a guide to investing. EA portfolios may contain specific securities that have been mentioned herein. EA makes no claim as to the suitability of these securities. Past performance is not a guarantee of future performance. Information contained herein is derived from sources we believe to be reliable, however, we do not represent that this information is complete or accurate and it should not be relied upon as such. All opinions expressed herein are subject to change without notice. This information is prepared for general information only. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. You should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. You should note that security values may fluctuate and that each security’s price or value may rise or fall. Accordingly, investors may receive back less than originally invested. Investing in any security involves certain systematic risks including, but not limited to, market risk, interest-rate risk, inflation risk, and event risk. These risks are in addition to any unsystematic risks associated with particular investment styles or strategies.

A great Christmas gift for parents and grandparents! A workbook to state the legacy of one’s beliefs, ethics, values and history to pass down. As a financial planner and advisor, I’ve assisted people with their estate planning for well over 30 years; how to prepare our possessions and financial assets to pass easily to our loved ones and charities, but what about our intangibles? Our knowledge? What is in our hearts? Within this workbook are questions to trigger or inspire you on various topics such as impactful life lessons, humorous family stories, good advice from your parents, and things you wish you had been taught! This is your love letter to those who live on after you and even those who aren’t born yet. On sale now on Amazon. Just click on the image below.Kasey Claytor