Life throws us small and large challenges. That is true whatever your background is, wherever you live, or who you are born to. One of the main tests in life is how you react to it.

All this recent news has me wishing I could just sell my children’s book and live in that world. But that wouldn’t be fair to all of our dear and valued clients who expect to hear from us during bad times as well as good times. As you should.

So, the stock market is appearing to fall into the basement. Where is the bottom? When will it stop? Will we lose our assets? And when will this virus recede? What will happen before it does?

No one knows the answers to these questions. The biggest clue to the future we have is found by looking at what went before.We have been here many times! Since I began my career in this financial industry in 1983, I’ve seen this type of situation many times: epidemics, pandemics, bear markets, and market corrections. And this is true: they are temporary. The markets recover. The viruses go away.

What is different is the modes of communication. The wide spread use of social media, the insidious use of news media continuously ramping up the use of alarming terminology when reporting information. In the 60s breaking news was used for an assassination or a huge global event. Now breaking news is every five minutes. The stress is high. The benefit is to the advertisers who know you’ll feel the need to continue to watch to prepare for some horrific future.

The short-term moves in the stock markets, (those less than 1 year, or even 3 years) are based more on emotions: fear, greed and hope, or guesses, than reality. Traders are constantly guessing what is around the corner. Most often they are just shooting in the dark.

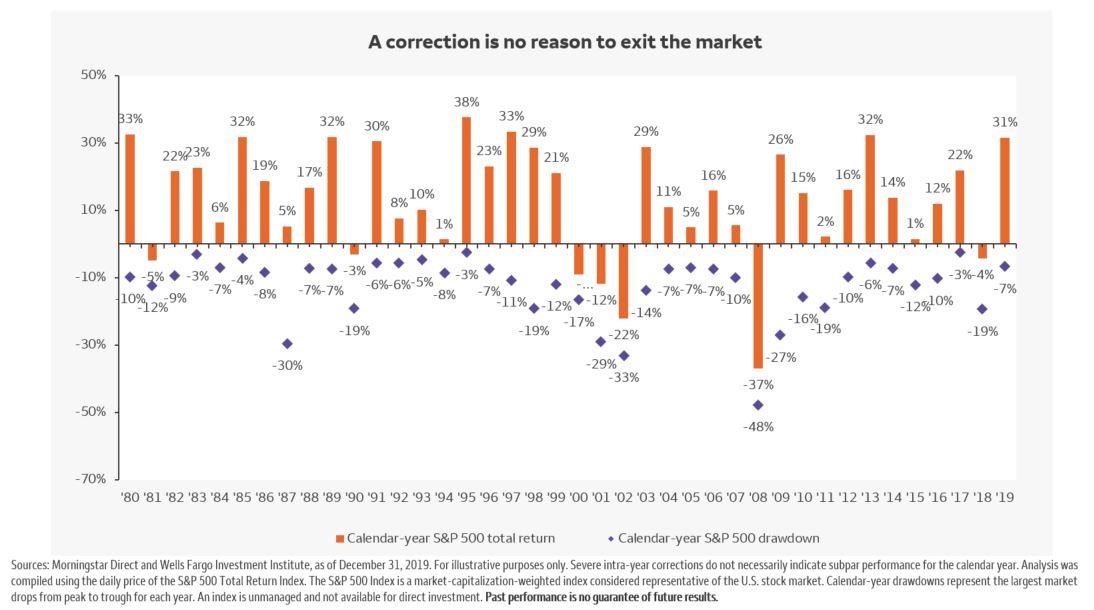

We have always cautioned to ignore these short-term expressions in the markets. When we look year over year, we see a calmer vista, a long expansion of growth. I’m including a chart that illustrates how the stock markets fall within every year, sometimes a small amount, sometimes pretty deeply, but over the years the declines are filled in, made up, risen out of.

I will tell you a little story. We stockbrokers all sat at our desks one Monday in October in 1987 completely stunned, paralyzed, because the markets were in what appeared to be a free fall like we’d never, ever seen. It was the largest percentage one day drop in history (-22.6%). That week we were dazed and afraid. But I did know the worst thing I thought I could do was to sell into this horrible market. Brokers, money managers, financial advisors, whatever you label those in this industry, do have emotions too.

One of my coworkers panicked. He sold and went to cash that week in his own 401k. We had about the same amount in our 401ks, we had been hired the same year 4 years earlier. The markets rose again, of course, and sometime during the recovery, he went back into the market. But he had lost so much, and being out of the market when it was going back up he never was able to make up for the losses he took selling at that time.

What a lesson for me as a young, green broker. I never forgot it. And I don’t want you to either.So hunker down, stay healthy and take care. Kasey

I do hope you can read the attached graph. It shows each years close in orange and the lowest points during the year with a purple diamond. Big drops are common, but always big news in the media. To Your Prosperity and Wellbeing,

Having walked my clients through planning, approaching, and living in retirement financially for the last almost 40 years, I couldn’t help but pick up on other aspects facing us besides the money part, such as grappling with when to retire, what to do in retirement, and how to plan a full and thriving last third of life? As I heard someone say; what are you going to do between now and dead?

As we near our ‘golden years’, we observe our elders living in a great variety of ways, from scrapping by on social security, to cruising or flying around the world, and travelling between multiple homes. There is an undeniable correlation between financial health and satisfaction in the later years, but this doesn’t mean you need to be stinking rich.

A successful retirement appears to have several moving parts: financial, health and wellbeing, relationships, passions and purpose; and let’s face it, nearing death also brings in one’s beliefs and how they experience their own spiritual life. So how do we prepare ourselves for this last and significant period of our lives?

First, not planning for it or setting goals, not contemplating how you will live in retirement, can cause unnecessary suffering later on. With no plan, with no savings, with no interests outside of work, some retirees may end up spinning in their own exhaust, no where to go and nothing to do. This can be disastrous on the human spirit. Depression and other mental health problems can take hold, leading to unhappiness and even physical ailments. But let’s not dwell on this, because the fact that you are reading this means you are proactive, interested, and willing to learn. Yay you!

This topic could easily be a 400-page book, but I’m just going to give you the briefest of outlines here.

1) Financially

Never too early or too late to begin saving. Have your paycheck debited for your employer plan, or, have your checking account systematically debited to go into an IRA, as much as you can afford, and then a little more.

Invest in a broad, diversified portfolio with stocks and bonds, low fees and good, comprehensive management.

Beware if you have the tendency, like some parents of adult children, to financially help them to such an extent you harm your own comfortable retirement. I remember a client who borrowed against his home, and withdrew from his IRAs, to help a daughter who said she couldn’t find a job. He did this until he and his wife had to give up their plans on traveling with their friends in retirement. He died leaving nothing for his wife, and only after his death did his daughter go to work to support herself.

We used to say in the financial business in the 1980s, you needed at least as much in savings as your closest decade in a hundred thousand dollars. For instance, at 40 years old you should have saved $400,000, at 60, $600,000, and so on. Typical standards now in financial planning state it really takes much closer to one million to have financial freedom these days to enable no financial worries, and the ability to take care of all your needs. Yet, I have seen people retire with half that and get along just fine.

Of course, take good care of yourself. Eat a good, healthy diet with lots of fresh vegetables, fruits, nuts and lean proteins.

Get outside every day. Walk, bike, swim, play, explore, move. Take up yoga or Tai chi, dancing or some other social exercise. These good habits will be easy to follow into retirement. With good balance falls become much less likely among many other benefits.

Find a mindfulness practice you like such as meditation, contemplation, breathing techniques, prayer and self-reflection etc. Conditioning the mind for wellbeing is also essential.

If you do have anxiety, depression, or other emotional problems bothering you, find a good therapist. Most of these issues are resolved with the proper help. Our society still attaches an unfortunate stigma to getting assistance in this area, but it is so essential, shows emotional maturity, self-care, and can be a rewarding experience.

Develop a positive attitude toward aging and retirement. Day dream about all the activities and experiences you’ll be able to enjoy, and the friends and family to spend time with. If you don’t have a close circle of friends, join a club or a class. Get involved in something you enjoy, sports, a book club, knitting, hiking etc. and read, I can’t stress how much reading can enhance anyone’s life in so many ways. There are so many great books in the self-help genre, but even a great book of fiction is a positive experience.

Cultivate peace with your own passing. Our cultures in the West have a poor record of coming to terms with death. It’s not usually spoken about except in dramatic and negative ways; we pretend it isn’t inevitable, we try to extend the lives of our loved ones in often grotesque and extreme ways, making their last days, weeks or months, lying in a sterile facility hooked up to machines and on heavy medications. My recommendation is to have a good plan. Most states have a type of Dying with Dignity form to fill out describing what you want done and how in a terminal situation. Email us if you would like us to mail you one. Other than this, building a solid belief of your own, whether religious or faith in life and nature, can re-frame the end of life as something not to fear. There are many great books on this.

3) Relationships

Fostering good relationships takes time, effort and the ability to forgive—maybe yourself or others. We all say or do things we don’t mean at times, are hurt by others words or actions, and without processing through these productively, we can be emotionally drained, hurt or worse. Forgive yourself and others. I know it’s hard. I will never forget a ninety-six-year-old, long-time client on his deathbed telling me he had been too hard on his wife and children. He was verbally abusive. He carried this all of his life. If he had been self-reflective, brave enough to look within, and been able to forgive himself, he wouldn’t have been so full of pain at the end.

Approaching this last stage of life, we can take the opportunity to develop a positive relationship with ourselves and others that will nurture us.

4) Passions and Purpose

What do you envision doing during retirement? So many people have jobs they don’t really enjoy, and so they dream of retiring as soon as possible, looking forward to having endless free days, like permanent weekends. But they’ve spent little time thinking about what they will do in retirement. I’ve seen some retire in their 50s and become bored, aimless and searching. Some go back to work. Some actually lose interest if life. On the other hand, I’ve seen people in their 70s who have no intention of retiring anytime soon because they love what they are doing.

Studies show the more control you have over what you do at work, who you work with and so on, the more satisfied you are. I believe that is why entrepreneurs often scoff at the idea of retiring, they are already living the life of their dreams.

To discover what your perfect retirement might look like, create a vision board of activities and places you’re interested in exploring. Think about what you enjoyed as a child.

Ask, how you may serve your community?

5) Deciding When to Retire

So, I am guessing you are beginning to see its not just at what age you can fiscally retire, it is so much more than that.

One, you want to retire when you are healthy and able to enjoy your passions

Two, you’ve figured out how you are going to fulfill your needs for community, purpose, interests and activities.

Three, make sure you aren’t just continuing to work because you have no idea what else to do with your life. Maybe you aren’t totally satisfied with work, but haven’t invested the time to explore what else might interest you.

Four, what about semi-retiring? This is getting very popular for those who have this option. And if you don’t, perhaps you could retire and pick up a part-time job doing something you’ve always wanted to do, like teach art or be in a counseling position.

Five, talk with your financial advisor about the income you will need during retirement. Take in to account how much your desired lifestyle will cost, your social security, and the amount of investments it will take to produce the income.

All of these subjects require some introspection; knowing yourself well will help you plan your later years to your benefit. Settling in to the idea of being an elder in the community, offering your hard-wrought wisdom, having loving relationships, enjoying the fruits of your labor, knowing how to still play, and exploring the world with a sense of wonder, can make your retirement the best time of your life.

Investing in stocks and bonds and having adequate insurance coverage is essential to any comprehensive wealth accumulation plan. The stock market has historically grown at a faster rate than inflation. So why do so many people have such poor results in their portfolios?

IMPATIENCE

Stock markets are cyclical. When one category of securities falls (such as large US company stocks) investors get nervous and make an emotional decision to move to another category that may be moving up at the time, (such as government bonds, for example). We instinctively want to move away from what seems painful. The mistake is that your investments often don’t respond the way you hope from this type of behavior.

In actuality, if you keep moving your investment from one type of security to another, it will erode the potential return because it will likely be in a market that will experience a down turn when the original US company stocks experience its next big move up! Truth is, no one really knows which sector will bring the best results and jumping around rarely produces positive results. Patience does.

HISTORICAL PERFORMANCE

It seems logical to pick mutual funds and other managed investments by how well they have performed in the past. It feels comfortable and looking at the data gives us the sense that we can predict how it will perform in the future.

Truth is, predicting future performance based on past performance has created loads of unhappy investors. Studies show the vast majority of funds DO NOT out-perform the market. Picking 100 or 150 stocks out of a stock market that has thousands of choices results in a very small chance of outperforming the broader market returns.

LACK OF DIVERSIFICATION

If you have 10 different mutual funds you may think you have good diversification. After all, you hold so many different funds, right?

Maybe not. These funds could have the same individual stocks in them, which means duplication – plus, there could be gaps in the portfolio – and the next good return is in a category you don’t even own! The next cyclical downturn in stocks could weigh heavily on your portfolio if you aren’t balanced among several markets.

Life happens pretty fast. Most of us are busy working away, adding to our retirement accounts in a company plan or an IRA. Before we know it, we’re nearing retirement. And there is something I’ve noticed about this.

It isn’t hard to build up our retirement if it’s taken out of our paychecks or checking accounts automatically. We don’t ever really miss it. But we may not find it so easy to do this with our after-tax money. Setting aside money for emergencies, other long-term savings, ready cash for vacations and big ticket items is important also. We’ve grown accustom to instant gratification, impulsively buying things we don’t need, and we whittle away the money we could be saving in a savings or investment account apart from long-term retirement ones.

In approaching retirement, many people find they have a nice amount in their IRAs or retirement plans, yet not much elsewhere. Once in retirement, or unluckily, laid off, they find they need to not only depend on an income from the retirement accounts, but it also is the place they need to go for big expenses such as repairing big items, needing a new a/c unit, or other big costs. And if they turn 70 ½, now they have to take a significant amount out for their RMD, (Required Mandatory Distribution), because the IRS wants to tax that account you’ve had great tax advantages on for so long.

One scenario: George has $1,000,000 in his IRA. He turned 70 ½ this year and must withdraw $50,000 and pay taxes on that. He may not need it, but he has to take the distribution anyway. He could have directed some of those savings to non-retirement accounts.

Another scenario: Harry, 55, has saved $300,000 in his IRA but has only about $7,000 in savings. He needs a new roof that will cost him $15,000. He needs to take it out of his IRA, paying income tax and a 10% penalty because he is not yet 59 ½.

The advice here is, in addition to saving for retirement, it is important to set aside other monies that is readily available without penalties or tax consequences. There are several ways to set this up automatically, much like your retirement plan at work.

Ask your employer if they have an after-tax savings plan you can contribute to that is reasonably accessible to you.

Set up a savings, money market, or mutual fund and direct your bank to send to this account a set amount at regular periods. Could be around your paycheck deposits.

When you sit down to pay your bills make a point to pay yourself first. Transfer money from your bank account to your savings online.

For extra windfalls such as a bonus, monetary gifts, inheritance, etc. save a portion.

There are more ideas, see if you can think of some. Just be aware so all your assets aren’t in a retirement account. Retirement accounts are for retirement income down the road.

Get with a financial planner and figure out a plan that will give you the income you’ll need in retirement and savings for needs while you’re working.

Lately it’s been more challenging out there, especially for older folks alone. Sometimes they get talked into buying products they can’t afford.

Just recently one of our clients was so pressured by an intimidating salesman, she signed up for a water purification system she couldn’t afford. He even told her he would get fired if she didn’t buy it. It did turn out ok for her though, in the end. They can’t touch her retirement account or her home, so she is lucky.

Another client had a salesman in her home to learn about stairway chair-lifts and he was so overbearing he insisted on her giving him her brokerage statement! He told her how she was invested incorrectly and picked up the phone and called me! When she realized he had called me she got on the phone and told me what was going on. I told her not to sign anything and call me later. Fortunately, she is fine, didn’t buy it, and he is now fired.

These two instances were very close calls. One would have had to pay $8,000 and the other $13,000. I am not saying the products were bad or not worth the price, but these clients weren’t in a position to pay for them.

But both women felt intimidated, stressed, even frightened by these aggressive men. I know our clients can make good, solid decisions. But, if you are alone and think you may feel at all vulnerable if someone is trying to hard-sell you something, have a plan ahead of time. Tell a close friend or family member about the appointment. Better yet, have a trusted person with you.

Sit by your phone ready to call if you feel intimidated, and tell your contact ahead of time a prearranged word or phrase to come over, such as “Can I afford this?”

If you do feel like you got pressured into buying something you shouldn’t have, under Florida law you have 3 days to cancel the purchase. For those of you in other states, check your state’s laws.

Call your financial advisor or planner before the appointment to discuss what a reasonable, affordable purchase for you would be, especially if you’re not sure. Then, if the product is over that amount, be firm with your decision that you will not buy it.

If you have already made a mistake and want to find out if anything can be done now, we can see if any of our resources can help, but if not, don’t berate yourself, just know you’ve learned from the experience.

If you have a friend or relative who may be vulnerable in this way, sit down with him or her and come up with a plan if a desired in-home purchase appointment is coming up. Not all companies have unethical salespeople. I know there are many great people out there. Just please be careful.

Sometimes we don’t realize how much an aggressive salesman or woman can coerce us into making an emotional, disastrous decision. Preparing for an appointment with a salesperson includes checking ourselves for our own steadfastness in protecting ourselves, even if that means reaching out for help.

Here is a check list of questions to ask yourself:

1) Does he/she prognosticate and predict?

We’ve been taught to expect our experts to tell us what is coming, yet in reality no one knows. We must be prepared for all possible and unseen events to the extent we can be.

2) When the market makes a big move up or down, does your advisor suggest changes to your portfolio?

If so:

A) Why was it incorrectly positioned in the first place?

B) Were there commission charges on the changes?

Your portfolio should be allocated to weather any storm for your time horizon and your comfort level. After that it is just routine maintenance to keep the allocation aligned with your original plan. The only time this might change is when you have big changes such as marriage or retirement.

3) Do you receive education on how the markets really work from your advisor?

Is there an opportunity for clients to learn methods of investing including philosophies so you can discern what yours is?

4) Does your advisor talk ‘above’ you? When you listen to your advisor is he/she understandable?

If you don’t understand, does he/she re-frame the answer in a way that you do? It is important you know what you are doing and why with your investments.

5) Do you have a high feeling of trust? Do you feel good after talking with him or her?

This will be your experience when your advisor is also a good ‘coach’. Your emotions will invariably work against your success if they go unchecked. You may be tempted to buy and sell at inopportune times. The stock markets will always have drops of 20% or more, and our decisions during those times can easily damage our long term plans. It is important that you can voice your fears and concerns to your advisor so that not only are you heard, but hopefully you will learn the truth about the markets and not the latest media buzz.

6) Have you been encouraged by your advisor to have reasonable expectations?

Such as:

A) The markets will cycle through bull and bear markets. During the last 31

years we had 24 positive returns. Even during the positive years the average intra-year decline was 14%

B) The stock markets will invariably decline over 20% at some time.

Are you prepared to stick with your plan no matter what is going on in the world and the markets? This is a sign of a seasoned, well-educated investor.

7) Lastly does your advisor understand, when it comes right down to it, your success has more to do with your internal commitment, internal guidance and financial maturity than any other variable?

If you have no resolve to leave your money invested through the tough times, can’t resist spending more than you earn, or you haven’t devised a good way to save, no advisor can be of much help.